Technology strategy

Looking Glass: Tech trends for automotive and manufacturing

OEMs have lucrative opportunities to cultivate new revenue streams through Direct-to-Consumer (D2C) Sales of machines, parts, subscriptions and services. But OEMs are not in a position to seize these opportunities:

OEMs are realigning dealer networks, cleaning up their digital estates and mastering new technologies to create simple and comprehensive engagement that is mutually successful and profitable for owner/operators, dealers and manufacturers alike.

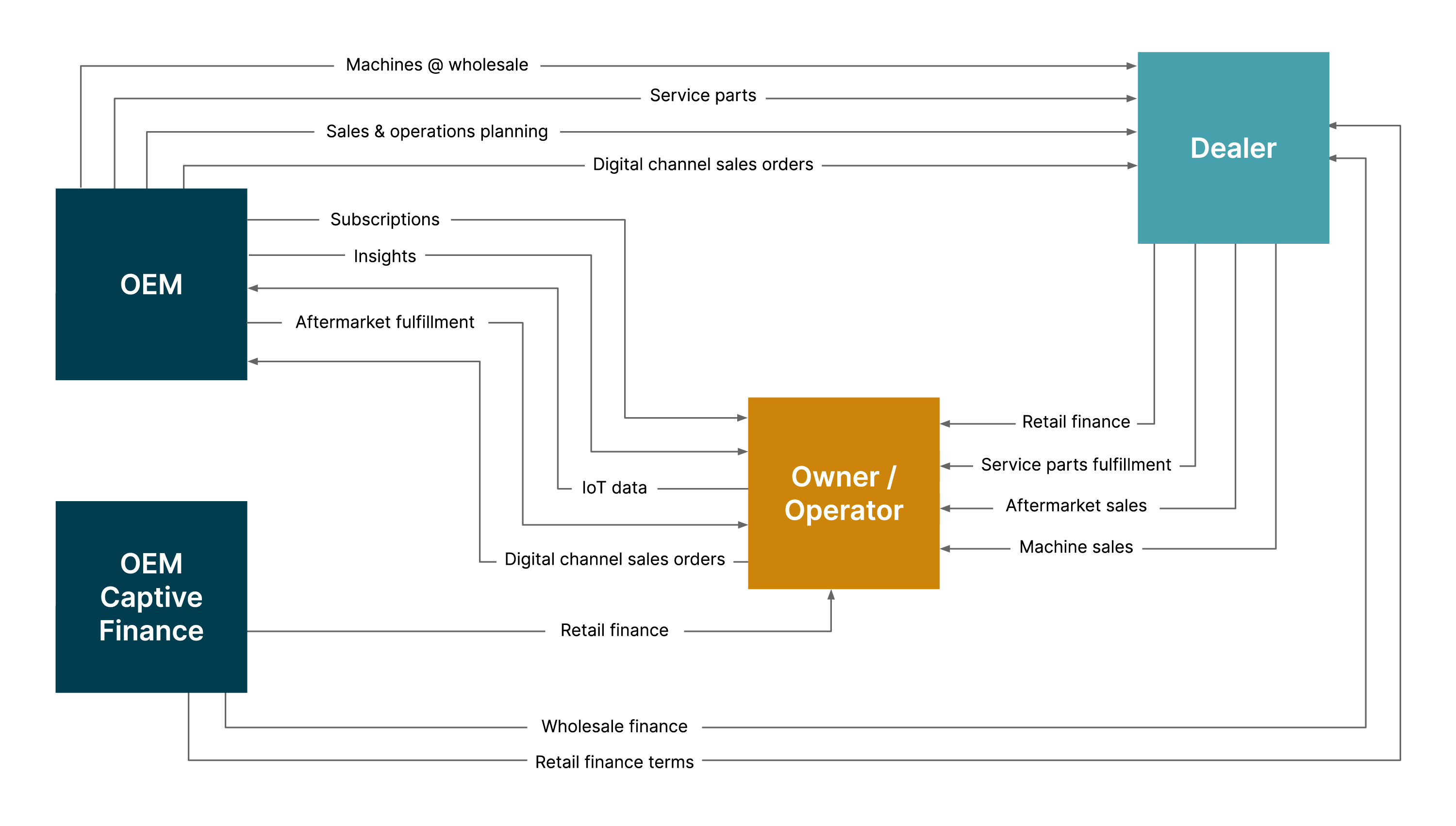

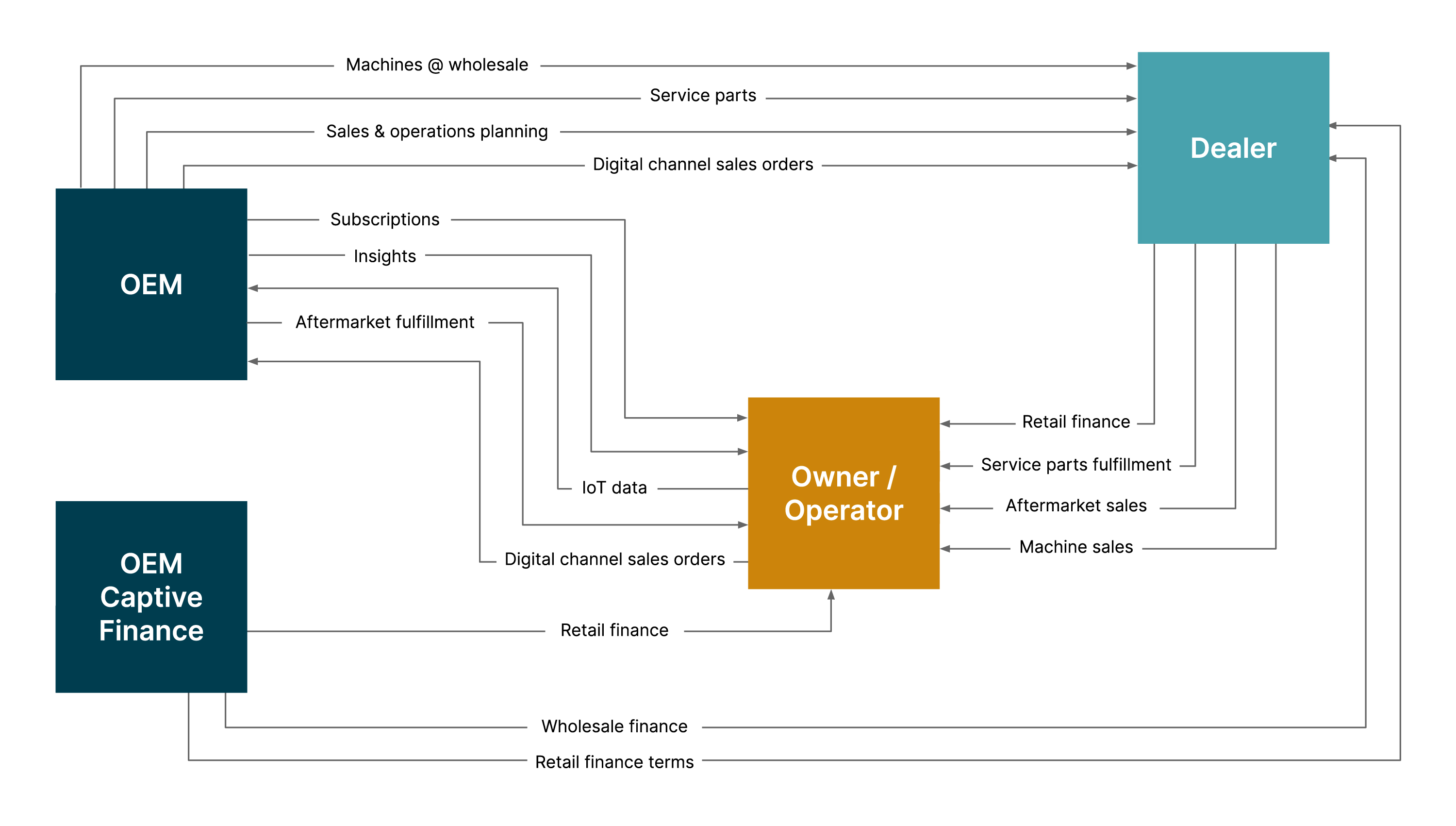

OEM revenue streams have traditionally been wholesale; manufacturers sell to dealers, who in turn sell machines and parts to owner/operator customers. That revenue profile is changing.

Machine-as-software allows OEMs to charge customers directly for enabling advanced machine capabilities. Increasingly complex machines make it less viable for owners or 3rd-party technicians to provide service. The direct sales model employed by electric vehicle OEMs yields profit margins that the traditional sales model simply cannot match. Investors welcome these changes because they promise revenue streams that are less vulnerable to the credit cycle, as well as higher and more consistent cash flows. It is no surprise that OEMs—from consumer durables to industrial machines—continue to invest in D2C channels for product and subscription sales, as well as leasing, finance and aftermarket.

Executing this shift requires that the sales channels (specifically, dealerships) be on board, but there is resistance. Dealers are not excited to choose wholesale over the retail premium they've pocketed for decades, nor are they willing to be disintermediated in the relationship with the end-customer. Dealers bound by territorial agreements in real life (IRL) have found there are no restrictions on their ability to pursue business through digital channels, enabling them to capture more sales in the conventional sales model. Additionally, technical service roles are difficult to staff, particularly in North America. While it sounds great that dealers will benefit from a services windfall, their labor footprint (e.g., acquisition, training, salary, and retention) must be ready to capture it. Dealers know what they stand to lose much more than they know what they stand to gain.

OEMs cannot effectively pursue D2C without co-opting channel resistance to position all partners to benefit from new opportunities for growth.

Industrial product dealerships built for IRL are subscale in the digital arena. Dealer networks are also asymmetric, with only the largest of the large having anywhere near the economic power to challenge this change; resistance simply pits dealer on dealer for a low-growth source of revenue. And with the revenue-mix changing, dealer investment in innovations in pursuit of yesterday’s revenue is a waste of capital. OEMs have a difficult task to bring dealers into alignment. While OEMs are not abandoning their dealer networks, OEMs must compel dealers to modernize commercial and fulfillment activities if they are to achieve equilibrium of the new revenue-mix throughout the network. Unless OEMs do this, those networks will be an impediment to change.

It will also take effort to get customers to buy into this change. The processes, systems, economic model and corporate culture are geared for a B2B2C model, not B2C. Buying from dealers means the frustration of haggling but the satisfaction of buying at a discount to retail; buying from the OEM means no more negotiation and paying MSRP. Plenty of customers aren't too excited to rent capabilities of machines they nominally purchased, or to lose the power of decision as to who performs repairs on the equipment.

OEM-provided insights and recommendations for machine use and maintenance are no doubt valuable, but must overcome trust barriers. Few people respond favorably to being watched or “graded” by anonymous people—or worse, by algorithms. It is out of the scope of this analysis, but suffice to say OEMs have their work cut out for them to be sufficiently transparent with customers so that D2C practices are not deemed predatory.

D2C doesn’t come cheap. The shift from wholesale to retail brings new customer touchpoints, which—even with all of the self-service technology in the world—will require increased headcount for customer service and solution engineer roles. Meanwhile, inflation continues to drive increases in OEM employee salaries. An increase in headcount for difficult-to-staff roles, in an environment where salaries remain elevated, is not an attractive proposition.

Not to mention, OEM commercial models are built around dealers, not owner/operators. Plenty of ink has been spent by the chattering classes that companies must become “customer centric”, but for OEMs this is a very real transition. OEMs enjoy an asymmetric commercial relationship with a limited number of captive businesses, i.e., dealers who have little choice but to accommodate the OEM’s commercial idiosyncrasies and shortcomings. In D2C transactions, OEMs must win the owner/operator’s business every day, with every attachment sale, service part sale, subscription renewal, as well as the financing that underwrites the transaction.

To sell in any volume direct-to-consumer, an OEM must overcome the fundamental problem of being difficult to do business with. Established OEMs—from consumer durables to industrial machines—do business with a small number of customers in the form of dealers or resellers. This has allowed OEMs the luxury of not investing substantially in customer experience beyond the manufactured product itself. However, starving customer experience of investment is a well-established formula for failure in retail markets.

OEMs are evolving rather than deprecating dealer channels. This means OEMs will bear the cost of maintaining the commercial infrastructure to support both B2C and B2B2C interactions. If OEMs can’t bear the cost, the pursuit of D2C will be short-lived.

The defining characteristic of OEM “Customer 360” initiatives is the extent to which companies negotiate with themselves over their scope and reach. Bring the arguments to an end with the simplest reference implementation that will do. Do the same for other data families such as manufactured product (as built) specifications, customer operated (as maintained) specifications, and the like. Build an organization to bring these to “market” as data products. The fact that dealers and owner/operators are building models for everything from operations efficiency to service scheduling, and are often starved for comprehensive data, creates demand for secure data products beyond users internal to the OEM. Most of all, make it safe for anybody to surface data quality and completeness problems. Domain models and data products are theoretical, it’s the data that matters; if the data is garbage everything built around it will be garbage.

Domain models and data products are theoretical—it’s the data that matters. If the data is garbage, everything built around it will be garbage.

OEMs must be easy to do business with in absolute, not relative, terms. It’s one thing to require a dealer to navigate multiple endpoints, but asking a customer to do the same is another. If selling machines, integrate your consumer finance department into the transaction flow. For subscription sales, establish a clear and consistent “Call-to-Action” across all communication channels (e.g., website, email, text), and ensure a responsive, mobile-friendly experience. If you sell service parts online, your site-search should have the ability to serve up the best price and availability network-wide. If you facilitate the resale of customer equipment, make it simple for the customer to expose inventory for sale and take that equipment off their balance sheet once it’s sold.

All of these require integrating different parts of the OEMs business into customer experiences. It’s well established that the way to do this is through APIs, but APIs must be strictly implemented. APIs don’t help, and arguably make matters worse when there are dozens of APIs that essentially do the same thing. APIs must be demonstrably recomposeable and recomposed: the API to confirm available credit is the same whether it is being used to purchase a machine, a service part, or renew a subscription. Reconcile the API catalog to the domain model and rationalize as necessary. OEMs have a difficult enough time creating low-friction customer experiences. While APIs are essential in creating effective experiences, they can be inhibitors if created thoughtlessly.

Once past the hygienic actions, OEMs can focus on value creation. Value creation at scale comes through restructuring, enhancing and amending channels to change them from independent, narrowly bound entities into a network that yields a network—that is, exponential—effect.

OEMs have a good handle on labor composition as it pertains to supporting a reseller network, but getting into D2C will bloat payrolls to provide even minimal customer support. Generative AI has proven it is viable for keeping payroll expansion in check. It's also proving to be effective at navigating uncertainty and unstructured situations. For example, Generative AI solutions have been deployed to augment customer support staff to improve fidelity of issue resolution and accelerate resolution times, increasing the capacity of the human workforce. Generative AI has also been applied to solve complex and high-volume operational problems, such as manufacturing facility scheduling in the automotive industry, which is essential as OEMs shift from manufacturing for dealer inventory to instead manufacturing for customer specification. Externally exposed large learning models are potential self-service tools, allowing dealers and owner/operators to navigate OEM complexity, whether machine, corporate or network.

The good news is, Generative AI is turning out to be useful. The bad news is that too many OEMs are still in the very early stages of familiarizing themselves with Generative AI, and their explorations will be tested on customers in live labs of varying results. Investors have been inundated with Generative AI narratives for well over a year now, they will not be patient with laggard adopters.

Investors have been inundated with Generative AI narratives for well over a year now, they will not be patient with laggard adopters.

Manufactured products are complex. Service beyond basic maintenance is increasingly beyond the reach of owner/operators and 3rd-party service providers. This promises greater service revenue potential for dealers. But the services themselves are only a boon to dealers if they can hire, train and retain the staff to perform these services. AI can assist with service diagnostics, Generative AI with recommendations, virtual reality with immersive technician training, and augmented reality with technician support and data acquisition feeding AI assistants.

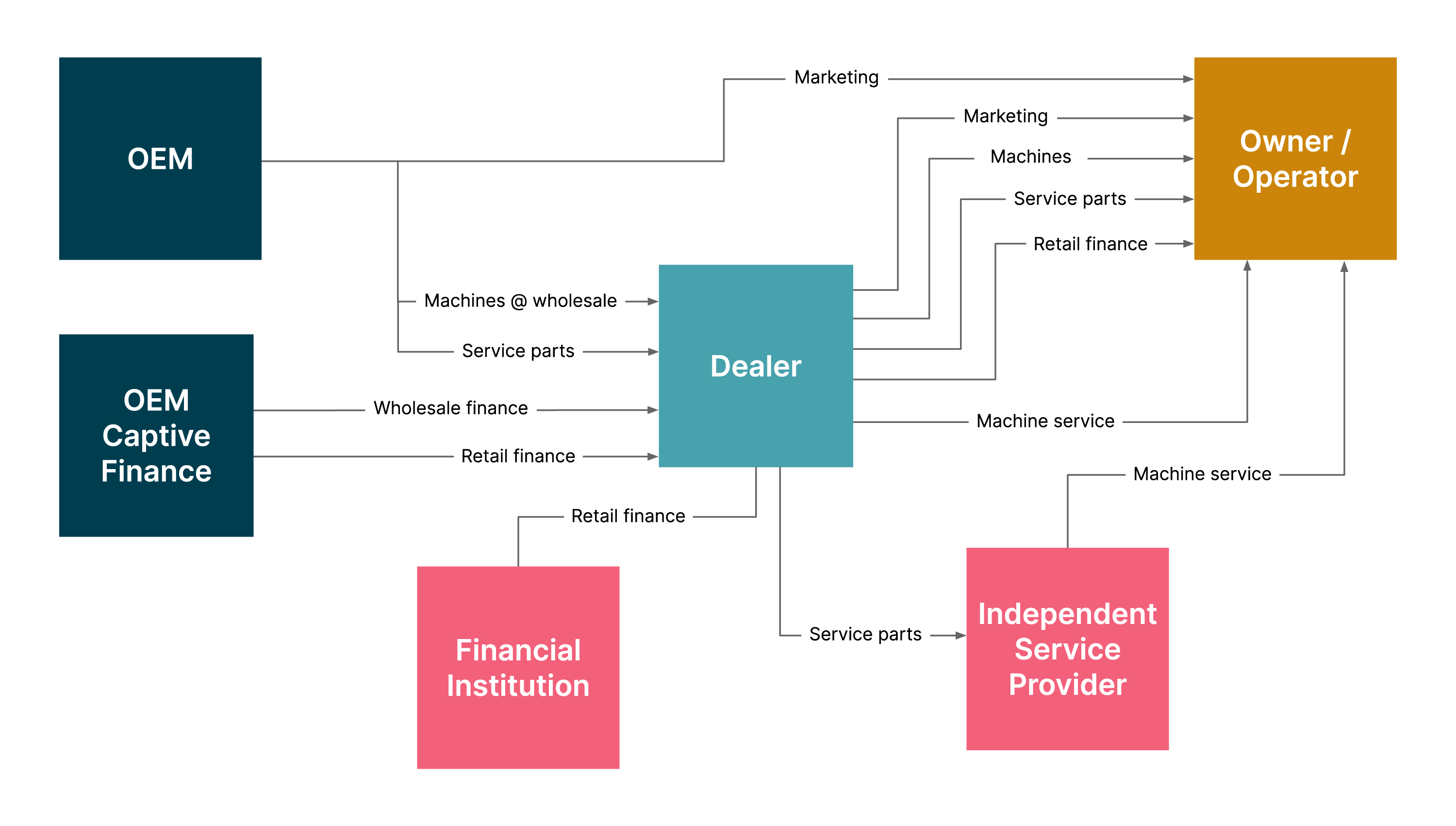

Expanding D2C comes with the responsibility for the OEM to leverage its network in its entirety—OEM and dealer inclusive—and make the navigation of the network transparent to the owner/operator. Forcing the customer to choose where in the network to check availability of service parts before purchasing them is unnecessarily complex and time consuming. It’s a hundred times worse if the customer is likely to wind up at a dead end in the channel they choose. Leveraging the network means augmenting dealers with captive customer distribution centers to backstop dealer-held inventory. These centers are optimized for the fulfillment of small-volume, high-priority customer orders for goods such as service parts, attachments and even small machines. The network is made seamless to the owner/operator through AI/ML-driven order routing which puts the customer order on the most efficient fulfillment source—dealer or OEM facility—for price, availability and cost to serve.

Dealers also provide essential machine service. As machines become more complex, service gets out of reach for the owner/operator and independent mechanic. This doesn’t just increase the dependency on dealer service, it means dealer service operations are a critical path to resolving machine down conditions—situations that are extremely expensive and potentially damaging to machine owners. The availability of service technicians becomes that much more integral to machine uptime and, therefore, customer success. IoT and advanced analytics that generate service notifications to product owner/operators are adaptable to the forecasting and scheduling of service events, extending sales and operations planning to include machine service visits. This expands the OEM scope of responsibility to include managing and optimizing dealer service operations for the benefit of owner/operators and dealers alike.

Complex, connected machines twined with accumulated customer data means every OEM is in the insights business. Insights are a means of driving more productive use of a product and scooping up aftermarket revenue. Insights are compute and data intensive, and the customer-facing insights product makes them labor intensive as well. Generative AI renders insights less burdensome, creating the opportunity to commoditize highly customized insights and opens the door for new families of insights. For example, OEMs can use Generative AI to compare IoT data against machine specification to spot maintenance issues, and against contemporary machine specification data to recommend upgrade (capabilities-as-software) or replacement, with a financial analysis of total cost of ownership of new machine savings and trade value when financed via the OEM. This usage and customer data can be scaled across an entire fleet for aggregate recommendations, creating an opportunity to increase customer lifetime value.

Servicing a customer through an established digital channel has negligible cost to the provider. That channel can have extremely high cost to the customer if it takes more time to arrive at a solution. It is also more costly to the customer if the solution that digital channel arrives at is no better, or more expensive than well-established analog channels. D2C channels must be demonstrably superior to the customer before they have any chance of delivering benefits to the provider.

D2C channels must be demonstrably superior to the customer before they have any chance of delivering benefits to the provider.

Providers like OEMs typically justify their channel investments based on "cost-to-serve”, but this metric is misleading. If the customer cost-to-solve is materially higher when the customer engages a digital channel, they will simply not use that digital channel. Cost-to-serve is zero for traffic that never arrives. A better metric is customer-centric: "cost-to-solve”. OEMs must re-evaluate every digital channel in light of the alternatives that the customer has and assess the viability of those channels in that light. There are plenty of technologies that make it practical and affordable to upgrade the ecosystem of channels, it is only practical to do so if the foundation is in place. As mentioned above, OEMs have to get their digital house in order by sorting out fundamental data and domain problems of accessibility, quality and boundary. Doing this gives rise to both primitive and compound platform capabilities consumable by employees, dealers and owner/operators alike. These capabilities are the foundation of contemporary digital-first channels that yield a reduced cost-to-solve for customers and a reduced cost-to-serve for OEMs and their networks, containing OEM costs for executing a D2C strategy while accelerating the OEM transition to D2C.

Capturing revenue (and capturing it profitably) through D2C strategies requires that OEMs align their channels, clean up their digital foundations and bring solutions based on modern technologies to make the complexity easier for everyone—owner/operators, dealers and employees—to manage.

Disclaimer: The statements and opinions expressed in this article are those of the author(s) and do not necessarily reflect the positions of Thoughtworks.