This is the last article in a four-part series, where the authors share their experiences and insights on ushering technology-fueled innovation in incumbent financial services organizations. Here are the first, second, and third articles in this series.

“The main obstacles to improved business responsiveness are slow decision-making, conflicting departmental goals and priorities, risk-averse cultures and silo-based information. Technology can play an important supporting role in enabling organizations to become more agile companies.”

— Economist Intelligence Unit report on Organizational Agility

According to MIT, agile firms grow revenue 37% faster and generate 30% higher profits than non-agile companies. Yet most companies are nowhere near agile; they admit they are not flexible enough to compete effectively.

In a hyper-competitive world, cycle times for innovation are compressing every day. Large enterprises traditionally excel in optimizing existing business models instead of experimenting with new ones. However, in such a fast-paced environment, continuous innovation cycles are mandatory to keep pace with existing and emerging competitors.

This is a world where AirBnB has the same valuation as Marriott. Large financial services firms are under the same threat. Can traditional wealth management or legacy brokerage firms offer a basket of thematic stocks with one purchase, like Motif Investing? Can they come close to the ease of use and low costs that Betterment offers both retail clients and registered investment advisors?

If financial services firms want to answer yes, they will need a dramatically new approach to innovation.

Behind Organizational Inertia

Recently, we conducted an organizational change initiative for a very large global bank. Nearly all technology projects across the business had three distinct, disturbing attributes:

- There was a significant mismatch between what customers expected and what was finally delivered by IT

- The average project had a 30% or more delay in schedule, with corresponding budget overruns

- Concept-to-customer feedback cycles took more than 9 months for any new product idea

The bank spent an enormous amount of time detailing project requirements up front, and then spent far too long building any technology of value. By the time they had anything to show their customers, those meticulously detailed requirements had fundamentally changed. And because the team had not accommodated potential changes to requirements, no budget existed to deliver against those changes. The entire management system was designed to deliver on historical business conditions.

This predicament is extremely common, and is not limited to IT. The “waterfall” mentality pervades most functional areas. It lies at the heart of organizational inertia, sapping an organization of the fighting spirit it needs to take simple ideas and transform them to products and services that can drive growth.

We've previously discussed the root cause of this brittle lag: traditionally, technology value is measured on cost and cost savings, leading to defensive, procedural behavior.

Go Lean

Adopting lean principles can help organizations foster the practices necessary to manage an innovation product portfolio. Based on our experiences running innovation labs and working with clients across the world, we recommend the following 5 step process to unleash innovation in your organization:

- Shift from a project mentality to a product paradigm. While the change in mindset is difficult, it is fundamental for introducing collective ownership and decision-making within an organization.

- Break down large-scale, high-risk product development efforts into smaller, low-risk experiments. Craft and empower small, autonomous teams based on cross-functional skills and interests. Bring people together across silos and existing business lines and P/Ls. Hold them collectively accountable to a business outcome, not to a set of features to build (unless you want your best people to leave).

- Provide these teams with the budget discretion to quickly test multiple ideas in parallel. Ask them to double down on what works—and dump the ones that don’t—within a fixed interval of time (3-5 months).

- To be successful with such rapid experimentation, teams have to clearly define the problem and identify appropriate metrics to measure success.

- Collaborate early and often with stakeholders from technology, business, marketing, advertising, product, etc.

We have seen the success of these principles firsthand. During the engagement with the global bank mentioned earlier, we were able to reduce the cycle time by more than 30% by introducing key innovation practices for requirement gathering and sharing. By creating a shared understanding of the problems being addressed at the onset of important projects and programs, we saw better expectation management across multiple stakeholder levels.

Other financial tech companies have also found success with these principles. LMAX is a London-based fintech upstart promoting speed and transparency in Forex Trading. In 2013, it had over $1 trillion in trading volume. When the company topped The Sunday Times’ prestigious Tech Track 100 List in 2014, CEO David Mercer proudly stated that credit belonged to the people in his teams being slightly stubborn, with the courage and conviction to do things differently from the status quo.

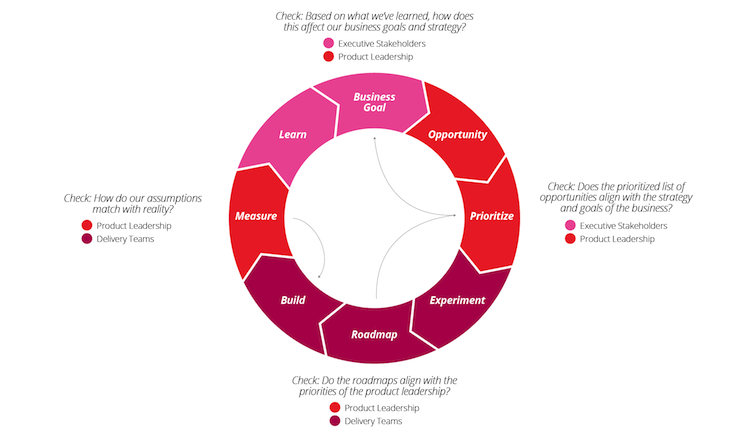

How to Integrate Lean Principles with Business Strategy

Adopt Cutting-Edge Engineering Practices

This kind of rapid adaptation to change also demands a change in the engineering practices to make sure that quality is not blindly compromised for speed.

WealthFront is a fintech startup that provides automated investment services. After just 3 years, it now manages over $2 billion in assets.

The Wealthfront engineering team uses continuous deployment and proportional investments to fix defects rapidly, deploying new software more than 30 times a day. By enabling the team to conceive, design and deploy new offerings quickly, Wealthfront has become the current market leader in providing automated investment portfolio management.

This is not folklore anymore. Organizations like GE have already created “growth boards” to significantly reduce the paper to production time. The company has been able to produce new products and services based on ideas from employees more rapidly than ever before. Once an idea is selected, employees are given capital and time to create a team and prove the idea is a viable future product or service for GE.

The Cost of Waiting

“The world won’t wait” for banks to catch the digital wave, says Richard Fairbank, the CEO of Capital One. Jamie Dimon of JPMorgan Chase agrees. For him, the biggest competitive threat to traditional banks is Silicon Valley and its prowess in consumer banking, payments, encryption, and verification capabilities.

Organizations cannot stay shrink wrapped by regulatory burdens and legacy IT. That path will fail to deliver winning experiences, or new products, to their consumers.

The message to senior leadership within large financial organizations is clear: break monolithic IT divisions into agile hubs that can respond to the rapid digitalization of every banking business line. The results of inaction are also clear: today's banks may not be tomorrow's banks.

Disclaimer: The statements and opinions expressed in this article are those of the author(s) and do not necessarily reflect the positions of Thoughtworks.