The investment management industry—and particularly, the advisory business model—is under siege. The combined forces of regulatory pressures, changing customer expectations and startups have put downward pressure on fees, increased the cost to serve and slowed down the growth.

Executives in every industry go through a phase of denial about their long-term viability, fully expecting to ride out storms through a combination of technology adoption, partnerships, and regulatory protectionism. Often unconsciously, industry conferences placate the fears of disruption by letting some untrue narratives take hold rather than providing a strong reality check.

At a recent financial services conference, one narrative centered on customer trust. Studies have shown that trust amongst the customer base is at a historic low for financial services firms, yet at the conference, the overriding hypothesis was that people ultimately trust people. As long as the bonds of human relationship were maintained, the disruptive threat could be averted, and customers were less likely to leave their financial fate in the hands of robo-advisors.

There are three problems with that narrative:

- Trust is a financial services industry problem

Trust is broken not just for the advisors, but for the entire financial services industry. Wealth management has the same poor reputation as insurance firms, banks, credit card providers, and even investment banking.

This hasn’t escaped the notice of the industry. Some conference participants also admitted that the advisory business has not always behaved in a trustworthy manner, so it’s always a challenge to win back the broken trust. The need for the recent fiduciary rule from the Department of Labour, which enshrines acting in the best interest of financial services customers, is symptomatic of this broken trust.

- Artificial intelligence is not an alien concept

People already trust algorithms over humans in their daily lives. Take Waze, the popular app that finds the best route for people to navigate to their destination (a dynamic GPS). People will soon be driving around in Google and Tesla self-driving cars, trusting their lives in the hands of technology to navigate dynamic road traffic.

Arguably, wealth management has lesser variables to contend with. It is also infinitely more scalable for an intelligent computer program to incorporate additional data than a human being ever can. AI technology is already becoming available quickly and cheaply (e.g. IBM’s Watson, Microsoft’s Project Oxford and Google’s TensorFlow), which has now been open sourced.

- Disruptive innovation starts at the low end of the market

Currently, robo-advisors are only attacking the low revenue end of the market and have an insignificant market share. Statistics from the Charles Schwab platform suggests that the previously self-managed investors are the ones who are making the transition to robo-advisors.

While robo-advisors have not yet made an adverse impact on advisor revenue, they point to a path for future disruption. Those familiar with Clayton Christensen’s Disruptive Innovation theory would know that this is an expected phenomenon. New industry entrants always make a dent at the price-sensitive end of the market, earning lower margins and serving a market that is ignored by the traditional competitors. These innovations then relentlessly move up the value chain and capture more mature and profitable markets.

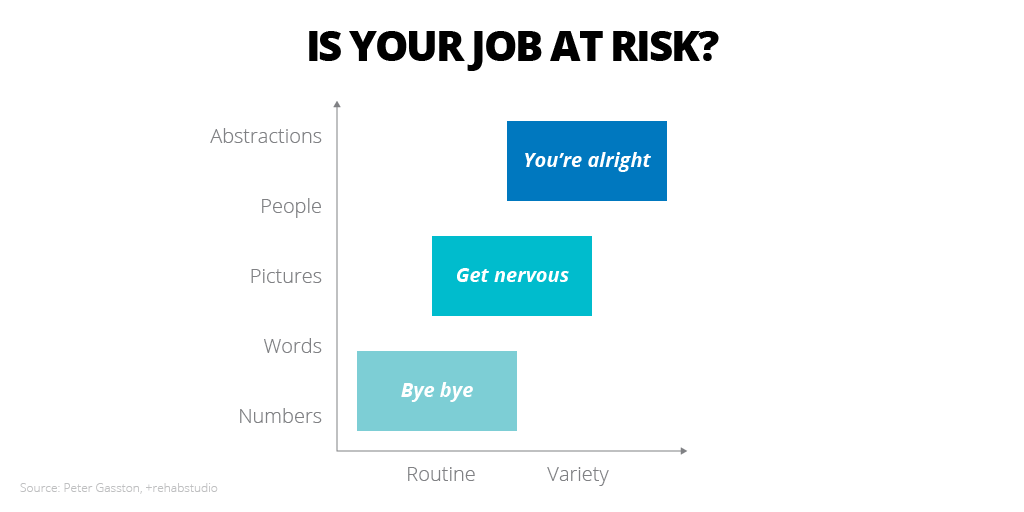

Does this mean that the advisor’s job is truly under threat? Here’s a neat graph that summarizes what is actually under threat.

This doesn’t mean that every wealth management firm should be rushing to build/ acquire the next AI platform. Clients are seeking transparency, responsiveness and stewardship from the advisors. To solve the issue of broken trust, firms will need to take a critical look at the value the client seeks.

In a subsequent post, we will explore the value question and how investment management industry can gear itself against the disruptive threats.

Disclaimer: The statements and opinions expressed in this article are those of the author(s) and do not necessarily reflect the positions of Thoughtworks.