AI and ML

Iress partners with Thoughtworks to accelerate platform modernization and AI-enabled growth in wealth management

TL;DR: The traditional 60/40 portfolio is losing its reliability, pushing more everyday investors toward alternative assets like private equity and hedge funds. But bringing these complex investments to retail audiences creates a massive operational burden for wealth managers. The firms that thrive in this new landscape will pair AI with human guidance: letting technology absorb the paperwork, while advisors educate clients on the realities of long-term, illiquid investing.

The idea of a structured investment portfolio is relatively new, germinating from the groundbreaking work of economist and Nobel laureate Harry Markowitz whose Modern Portfolio Theory (MPT) introduced the principle of constructing portfolios based on a client's risk tolerance, not just asset prices. From this, came the golden 60/40 rule of investing: 60% in stocks for growth, 40% in bonds for stability. This model enjoyed decades of dominance as a resilient all-weather strategy, underpinned by the historically low correlation between stocks and bonds.¹

However, the very assumptions underlying the 60/40 model can at times falter, as was evident in 2022 when the US Federal Reserve raised interest rates to fight inflation causing both stock and bond prices to fall simultaneously. While this signalled that bonds are no longer the reliable portfolio stabilizers they once were, it also underscored a more profound truth: relying on a two-pronged asset strategy is not sufficient for effective diversification and strong returns.

Today, investments navigate a fundamentally altered landscape defined by persistent inflation, subdued expectations for public equities and a shrinking pool of publicly traded companies. As a result, investors are naturally turning towards alternative assets like private equity, private credit, infrastructure, hedge funds and real assets as new sources of diversification, income and growth. Alternative asset investments have historically been concentrated among high-net-worth individuals (HNI) and ultra-high-net-worth individuals (UHNI), but they are now increasingly being sought after by mass-affluent investors as well. The trend is backed by scale: global alternative assets surpassed approximately US$16.8 trillion in 2023 and are projected to reach roughly $29.22tn by the end of 2029.²

However, this rise is not just being driven by capital influx. It is also being enabled by technology. AI-driven due-diligence and suitability analytics are reducing advisor burden; data extraction and portfolio aggregation engines are transforming opaque, multi-pager fund documents into usable insights; lifecycle automation and digital onboarding utilities are simplifying capital-call and servicing workflows, while tokenization, digital transfer agency and API-based ecosystems are lowering barriers to access.

For financial institutions, asset managers and wealth platforms, this convergence of capital markets transformation and digital acceleration presents both an opportunity and a challenge. The firms that succeed will be those that can seamlessly integrate technology with investment expertise by re-engineering operating models, scaling digital distribution and leveraging data and AI to unlock value across the alternative investments lifecycle.

While historically dominated by sovereign wealth funds and ultra-wealthy family offices, the surge in alternative investments across the Middle East is now experiencing a gradual democratization. The Gulf Cooperation Council (GCC) holding an estimated US$2.2 trillion under AUM³, is generating rapid growth in private wealth. A large and expanding mass-affluent investor segment, particularly in the UAE and Saudi Arabia, is increasingly seeking access to private markets to diversify portfolios and capture higher yields.

In the past, minimum investment thresholds of US$5 million or more kept alternatives largely out of reach for this segment. Today, technology is lowering both the cost-to-serve and minimum investment levels. Domestic and expatriate investors are also shifting wealth that was previously invested offshore into regional financial hubs such as the Dubai International Financial Centre and Abu Dhabi Global Market. These hubs have enabled feeder funds, private-market platforms and digital-asset frameworks that make alternatives accessible at lower minimums and through regulated wealth channels.

This shift mirrors global trends: alternatives are transitioning from an institutional asset class to a mainstream wealth management allocation, with the Middle East among the fastest-growing adoption regions.⁴

As more and more capital flows into private markets, investors are also expecting better digital experiences. Family offices and mass-affluent clients increasingly want real-time portfolio visibility, faster subscription and redemption processes, and more personalized reporting. This is creating strong demand for modern wealth-technology platforms across the region.

Beyond the burgeoning demand for alternative investments, there is a profound commercial urgency driving this shift. Fee compression in public markets is relentlessly eroding traditional revenue pools, leaving private markets as one of the last high-margin segments in wealth management. Consequently, firms that fail to industrialize their alternatives business today are not just risking operational friction, but ceding future margins and market share to more agile, technology-enabled competitors.

To capture this opportunity, leading firms are undergoing a dual transformation: a comprehensive overhaul of their technological operating models and a strategic upskilling of their human advisors. This is not a choice between technology or human expertise; it is a co-dependent ecosystem where one cannot succeed without the other.

The core challenge for wealth managers is no longer a lack of alternative products, but the immense operational complexity they introduce. As firms attempt to scale these offerings, the sheer administrative burden of the subscription and onboarding process is overwhelming advisor capacity.

Industry data reveals exactly where these bottlenecks lie: 66% of wealth managers cite obtaining and verifying investor data as a major time drain, and over 51% struggle with completing numerous manual fields.5 Bogged down by this relentless paperwork, advisors often default to simpler, traditional assets.

Overcoming this adoption hurdle requires targeted technological intervention such as automated digital KYC utilities and AI-driven data extraction to eliminate manual workflows and free up the advisor’s bandwidth.

Here is how a modern technology stack directly neutralizes these hurdles:

While technology streamlines operations, the human advisor still remains the cornerstone of client relationships. As alternatives introduce illiquidity, complex cash-flow profiles and long holding periods into wealth portfolios, advisors must move towards deeper suitability assessment, liquidity planning and lifecycle guidance, which requires new expertise in private-market structures and a more consultative, long-horizon engagement model.

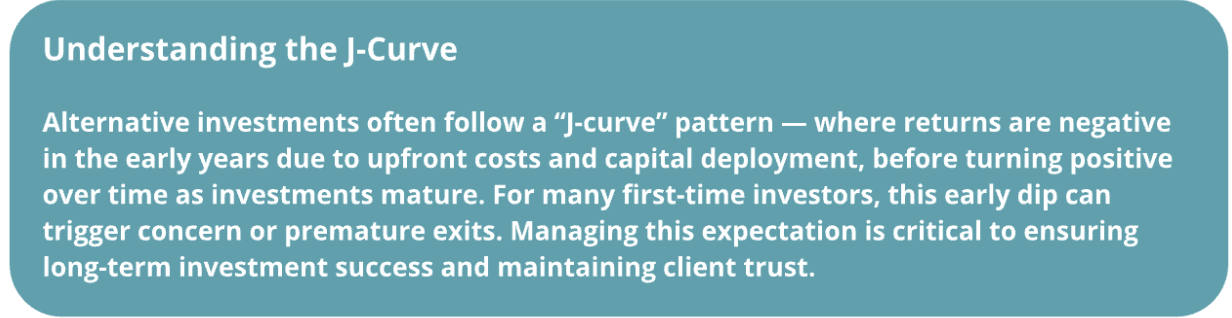

Many new investors jump into alternatives expecting the quick wins of the stock market. Advisors have to actively manage these expectations. They must act as educators: explaining the "J-curve" (where early returns often dip before they climb), preparing clients for multi-year lock-ups and keeping them focused on the long-term goal rather than short-term performance.

Determining whether an alternative investment is appropriate requires more than a standard risk questionnaire. Advisors must take a consultative approach: exploring a client’s prior experience, investment horizon, liquidity needs and income requirements. Questions about the balance between steady income versus growth, or sensitivity to fees and return expectations, help align strategies with individual goals. This human judgment — which technology can only support, not replace — is central to building lasting trust.

Given the complexity of alternatives, ongoing education is critical. Firms must invest in professional development and certifications that equip advisors to navigate diverse asset classes, from private equity and private credit to hedge funds and real estate. A culture of continuous learning is non-negotiable for firms that wish to remain competitive in the new era of wealth management.

The evolution of the modern portfolio from a simple two-asset formula to a complex multi-asset ecosystem represents a critical inflection point for the wealth management industry. The success of this transition hinges on a firm's ability to effectively integrate technology and human expertise.

The most effective path forward for wealth management firms is to:

Build for scale

Modernize core systems to handle illiquid assets, complex fee structures and long capital cycles unique to alternatives.

Harness AI to automate the complexities

Use AI-driven automation to streamline documentation, KYC/AML and compliance, which are areas consistently cited as more complex than traditional assets.

Elevate the advisor

Shift advisors from administrators to strategic consultants.

Redesign the client journey

Deliver transparency, liquidity insights and personalized reporting.

Partner for transformation

Collaborate with technology and ecosystem partners to integrate private-market infrastructure and cross-border regulatory capabilities.

The alternatives boom represents a once-in-a-generation growth opportunity. Firms that embrace this shift today will lead the wealth management industry into its next era.