Legacy modernization

Fortune 500 financial services organization

European banks are spending as much as 70% of their technology budgets maintaining legacy systems. At the same time, real-time payments are expanding, regulatory demands are tightening under frameworks such as DORA and the EU AI Act, and investment in AI continues to accelerate.

The pressure is building unevenly. Capital is moving faster than the infrastructure supporting it.

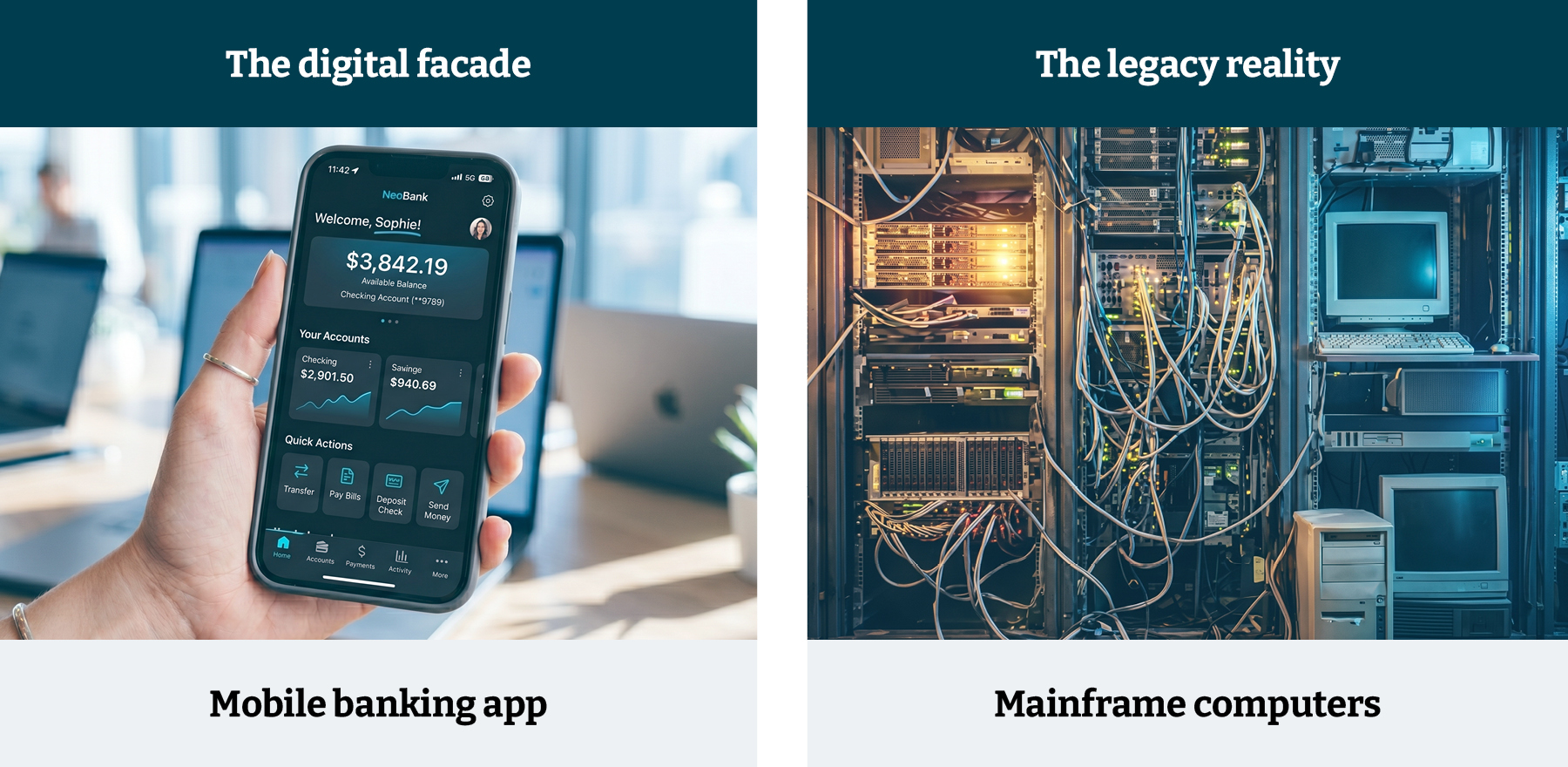

From the outside, most banks appear to have kept pace: digital interfaces, API ecosystems, visible AI capabilities. Internally, many are still running on core systems shaped over decades, with embedded logic that is difficult to trace and even harder to change.

These systems were built for batch cycles and manual oversight. They now sit at the centre of an environment that expects continuous, real-time execution.

That friction is now a critical problem. As AI shifts from offering advice to executing actions, allocating liquidity, routing payments and managing risk in real time, it exposes the "stranger core": infrastructure that works, but that nobody fully understands anymore. It hums along just fine, right up until it’s asked to adapt.

Before banks can even talk about modernization, they need basic visibility. You can't safely upgrade a black box. Trying to force AI-driven logic onto an unmapped legacy system guarantees expensive delays. Heading into 2026, flying blind like this is a massive risk.

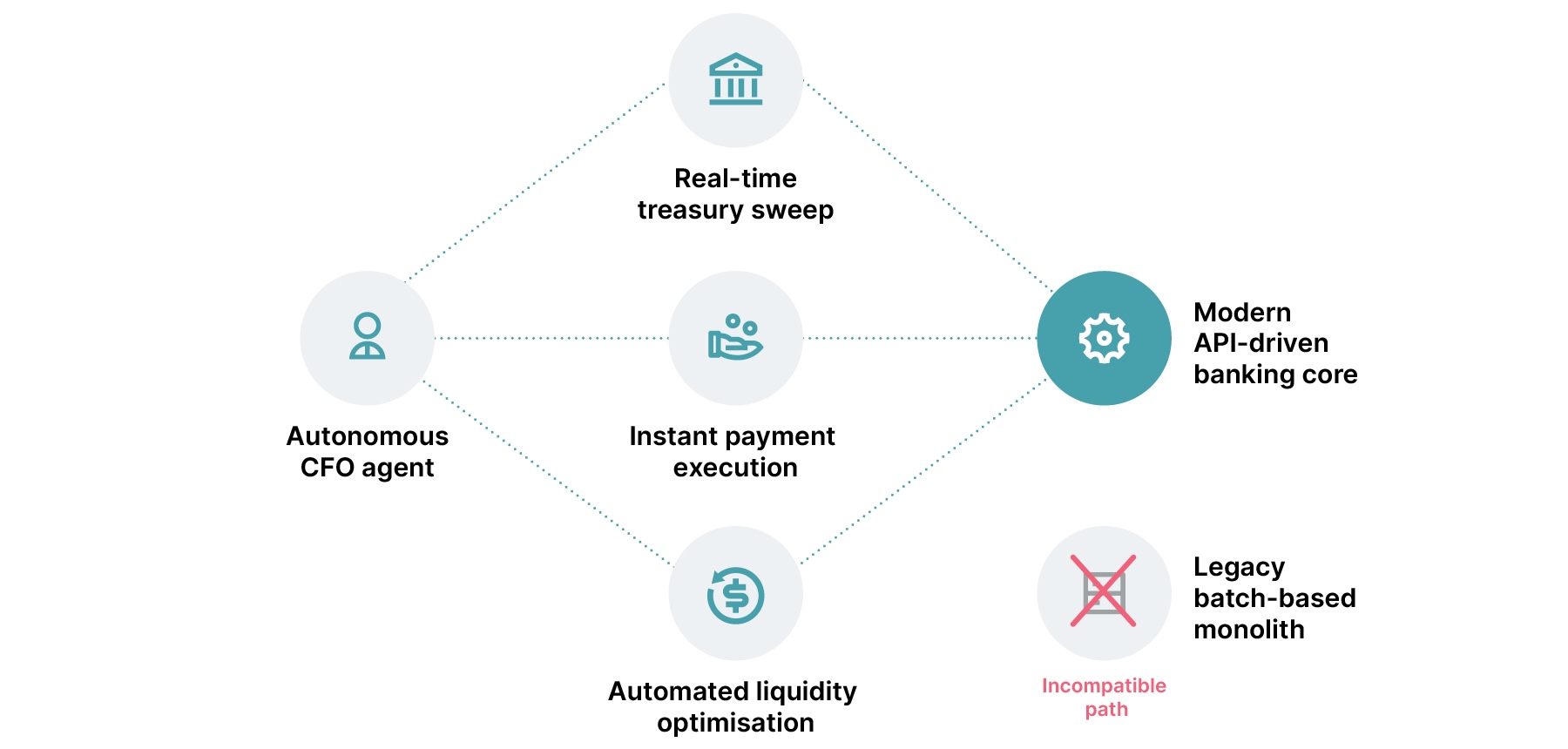

Corporate treasury is undergoing a quiet transformation. Decision-making is shifting from humans to algorithms, toward what can be described as “agentic money”.

In this environment, the limitations of legacy infrastructure become immediately apparent. A well-designed API cannot compensate for a slow, batch-based core. Autonomous systems do not negotiate or build relationships; they optimize. And they route around friction.

Even marginal delays can redirect significant volumes of capital. Where switching banks once required months of negotiation, it can now be triggered by a few lines of code.

To remain competitive, banks are being forced to prioritize high-value domains such as payments and liquidity, upgrading them for real-time execution. But modernization cannot proceed on assumption. Increasingly, institutions are turning to platforms like AI/works™ to map the actual logic embedded within their systems, rather than relying on outdated documentation.

The principle is straightforward: before rebuilding, you need to understand what already exists.

The idea of a programmable balance sheet is gaining traction. In practice, it depends on a single condition: full transparency.

Today, that condition is rarely met. Business rules are often buried deep within legacy systems, data lineage is inconsistent and automated decisions are difficult to trace. The result is a structural limitation — not only on optimization, but also on explainability.

A balance sheet cannot be programmed if its underlying logic remains opaque.

Some banks are beginning to address this by treating transparency itself as infrastructure. Rather than layering new solutions on top, they are using AI to uncover embedded logic, map dependencies and reconstruct how decisions are made across the system.

This shift establishes the foundations for what might be termed deterministic finance, where performance and compliance are more aligned.

In banking M&A, value is often determined not at the point of deal-making, but in the months that follow. Integration speed is critical, and when it falters, the root cause is usually architectural.

Legacy systems are rarely cleanly separable. They contain overlapping logic, duplicated functions and deeply intertwined data structures. Merging them without full visibility turns integration into a reactive and costly process.

A different approach is emerging. Rather than deferring architectural questions, some institutions are addressing them upfront, using AI to map both environments before integration begins.

This replaces assumption with evidence. Integration becomes less about stitching together opaque systems, and more about orchestrating modular components with a clearer understanding of how they interact.

As AI moves from insight to execution, governance can no longer remain retrospective.

Many banks still rely on after-the-fact controls, reconstructing decisions, auditing outcomes and validating compliance once actions have already been taken. That model struggles to scale in an environment where decisions are continuous and automated.

The shift underway is toward embedding governance directly into execution. Policy enforcement, monitoring and explainability are becoming integral to system design, rather than external overlays.

Approaches such as AI/works™ support this by enabling transparent model behavior and system-level explainability within modernized domains.

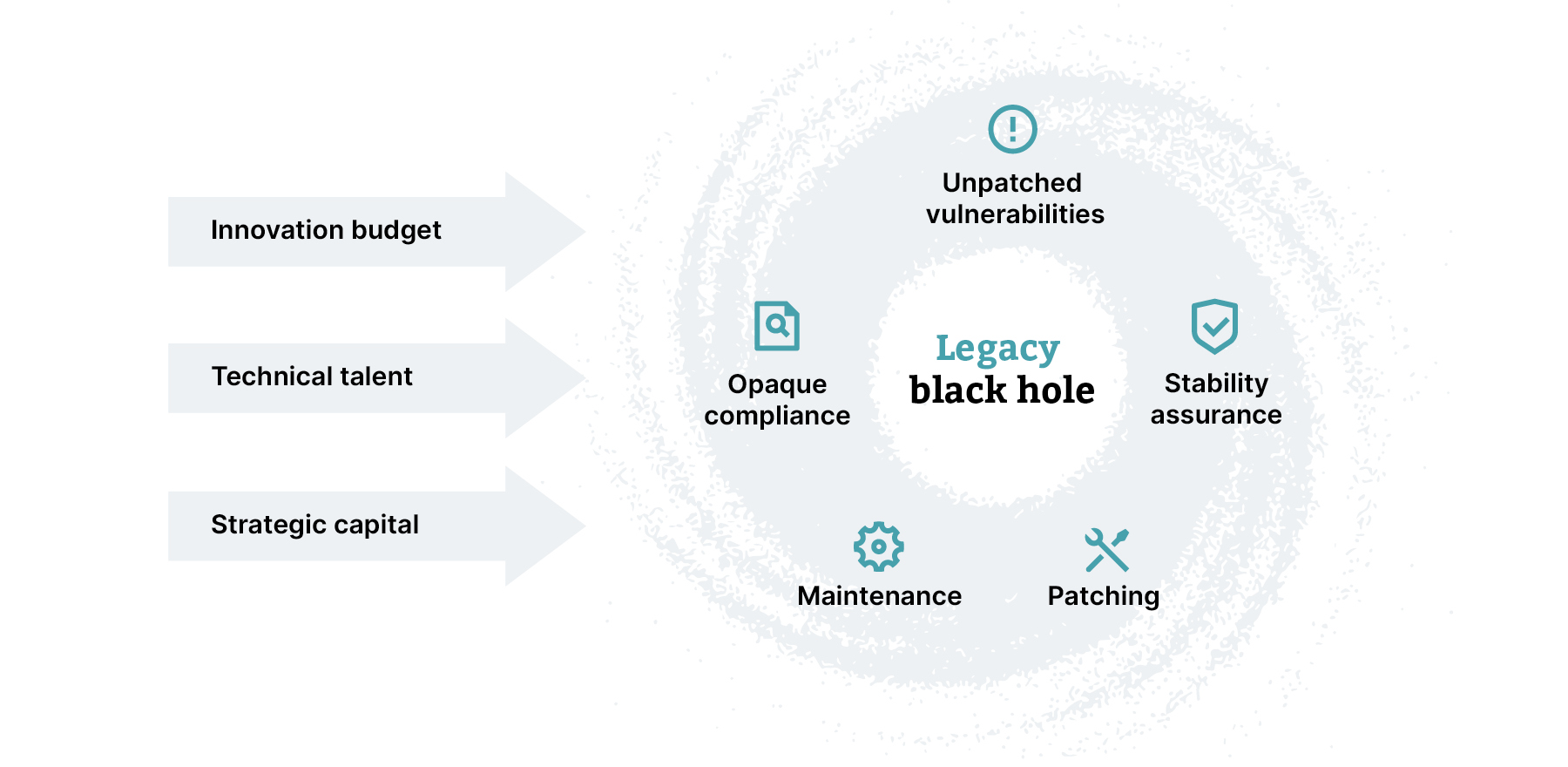

Cost pressures across banking are persistent, but often misdiagnosed. They are typically treated as financial problems, addressed through periodic cost programs.

In reality, they are architectural.

Duplicated systems, redundant logic and fragmented ownership create structural inefficiencies that cannot be resolved through surface-level interventions. Without addressing these underlying issues, cost reductions tend to be temporary.

A more durable response is emerging: simplifying at the design level. This involves clearer domain ownership, more modular architectures and the systematic elimination of duplication.

AI is increasingly used to support this process, identifying overlap, quantifying technical debt and enabling more targeted decisions. In this context, cost reduction is not the objective, but the outcome of greater clarity.

Taken individually, these five tensions can be managed within IT. Taken together, they point to a broader shift in how banks compete.

As capital becomes more automated and regulatory expectations move toward continuous resilience, performance will depend on how well institutions can operate at speed while maintaining control. For many, the limiting factor is not access to new technology, but visibility into existing systems. While high-level consultancy frameworks focus heavily on process redesign and workforce upskilling to prepare for this shift, they ignore a stark reality: you cannot upskill a workforce for agentic workflows that a batch-based mainframe physically cannot execute. Visibility is the mandatory engineering prerequisite to any competitor's strategy.

The “stranger core” is unlikely to fail abruptly. Its effects are more gradual and harder to isolate — slower execution, delayed integrations and capital flowing to institutions that can respond more quickly. This is where the mainstream industry narrative falters. Competitor perspectives largely treat the agentic shift as a front-office, productivity-enhancement story. But this isn't a matter of building shinier chatbots; it is a question of structural, systemic survival. You cannot safely encode governance boundaries or deploy autonomous agents onto an unmapped black box.

For the C-suite, this places architecture firmly in the realm of enterprise strategy. Decisions about the core now shape growth, risk and competitiveness.

Overcoming this architectural debt requires strict operating discipline: establishing clear domain ownership, governing emerging AI behavior at runtime and replacing retrospective compliance with real-time explainability. This transition must be sequenced deliberately, evolving the architecture domain by domain based on hard, verifiable evidence.

By 2026, the distinction will be clear: some banks will be operating on systems they understand and can adapt with confidence. Others will still be working around infrastructure that constrains them.