When public cloud technology first emerged, organizations across all industries instantly recognized the value it could bring to their business — and banks were no exception. Financial institutions the world over also began devising strategies to embrace public cloud and use it to transform virtually every aspect of their technology estate.

The ultimate goal for many of these banks was to become cloud-native — moving their entire digital core to the cloud to seize the full flexibility, agility, economy and scalability advantages public cloud can deliver. But for many, it’s a goal that’s yet to be achieved.

For most banks, cloud-native transformation has been challenging because of their complex migration approaches, industry concerns around security and fears of business impacting disruptions across their business. It is not uncommon, therefore, to find these programs stalling. Now, those banks are seeking new ways to realize the full potential and value of the public cloud. As the following case study highlights, full cloud-nativity for a bank is not only possible but immensely beneficial.

What cloud-native banking success looks like

One bank that persisted when faced with these challenges was Capital One. The consumer bank prides itself on its customer-centricity, and is singularly focused on transforming and optimizing banking customer experiences, a goal that public cloud is uniquely able to support and enable.

Capital One started its cloud journey by moving to private cloud infrastructure in 2013. The following year, it began its shift to public cloud. This incremental approach enabled the bank to do a lot of the hard work upfront, which helped create and maintain momentum for the transformation. In 2019, Capital One became 100% public cloud-native — shutting down the last of its eight data centers.

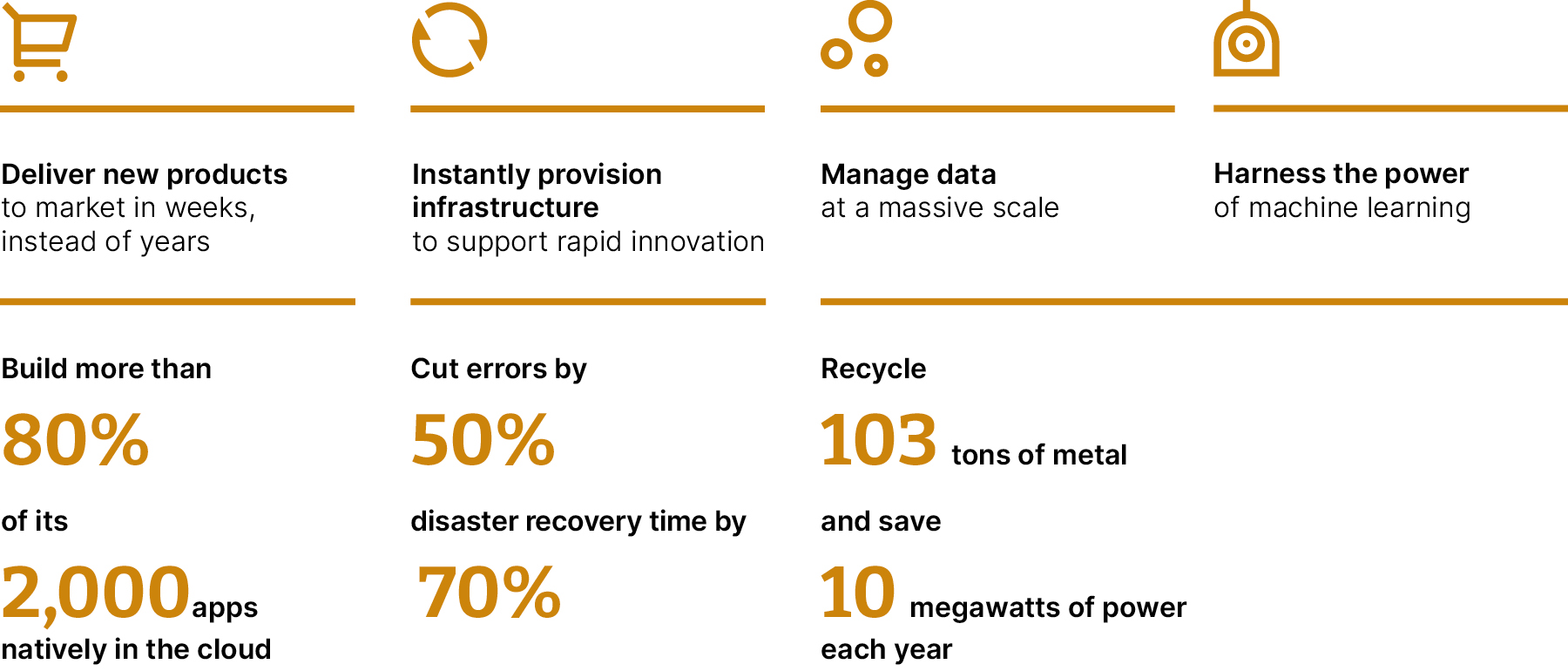

Almost immediately, the bank began to realize huge operational benefits:

Capital One's cloud journey

Why is public cloud such a good fit for banks?

Capital One’s story is inspiring, but it’s far from unique. Public cloud can deliver similar value for virtually any bank anywhere in the world, because it’s so well-aligned with banks’ two overarching goals: building consumer trust and maintaining a financially sustainable institution.

To fully understand the deep resonance between cloud nativity and banking, we need to break those goals down further, and explore how becoming 100% cloud native supports the diverse tasks that help banks achieve them.

Building and maintaining consumer trust

In banking, consumer trust is a complex concept that’s influenced by a huge range of factors. To simplify it slightly, we can say that on the whole, consumers trust banks that:

Are always available where and when they need them

Have a strong security track record

Proactively comply with existing and emerging regulations

Are demonstrably financially sustainable

Here’s how becoming cloud native directly supports the first three:

Resilience and availability

Cloud native architectures are made up of modular and decoupled services. So, if a particular service or subsystem fails, its impact is limited and contained. For customers, this means that an issue with a single capability (such as loan management) doesn’t impact their ability to access other features (like payments or transfers).

Security

Cloud native architectures promote ‘zero trust’ security, where banking services, products and operations are secured individually with fine-grained access control. Those controls are implemented as codified policies, which makes them easy to manage centrally and audit transparently.

Cloud providers also work with a ‘shared responsibility’ model for security. While banks remain responsible for maintaining the security of their applications and data, cloud service providers are responsible for maintaining the security of cloud infrastructure. Most providers invest substantially into making their infrastructure as secure as possible — achieving a level of security far beyond what most banks could maintain by themselves.

Compliance

Another area where working with cloud providers benefits banks is compliance. Market leaders like AWS provide a range of services for governance and compliance in financial services. These help reduce the substantial technical heavy lifting associated with achieving and maintaining regulatory compliance.

As banks shift their focus towards complying with emerging open banking requirements, cloud platforms can help them access the capabilities they need to build and expose secure APIs with ease.

Maintaining a financially sustainable institution

The fourth point on that list — the need to maintain a stable and sustainable financial position — is a major goal in its own right and needs to be broken down even further to fully understand the ways public cloud nativity can support it.

Public cloud helps banks maintain financial sustainability in two key ways:

Scaling costs on-demand

Banking – and retail banking in particular – is a seasonal and cyclical business. Seasonal events and payday weeks bring surges in demand. But when they rely on on-premises systems, banks only have two options to manage those surges:

Queue requests and process them in batches over time — delaying what customers have asked for

Provision capacity upfront at the level required during demand spikes — resulting in overprovisioning at all other times

In the cloud, capacity can be dynamically scaled as required. So, when demand spikes, banks can quickly, and usually automatically, add the capacity they need to execute customer requests immediately. Then, when it’s over, they can quickly scale capacity back down to avoid overspending.

That sounds like a marginal gain, but across a bank’s operations that scalability can free up a huge amount of capital that can instead be invested in growth and value-adding activities.

Agility and flexibility

In an industry increasingly shaped by agile fintechs that are highly responsive to customer needs, banks must do all they can to bring new products to market quickly. The scalability and instant provisioning delivered in the public cloud empowers banks to build and launch cloud-native apps and services incredibly quickly.

Plus, if a service stops delivering value, banks have the flexibility to quickly shut that service down, and put those resources into something new that’s better aligned with customer and business needs.

What’s keeping banks from the cloud?

Today’s leading neobanks and fintechs are harnessing the power of the public cloud to inspire consumer trust and build financially sustainable institutions. So why have so many incumbent banks struggled to do the same?

The biggest barrier to public cloud transformation that most traditional banks cite is that unlike their agile, emerging competitors, they aren’t starting with a blank slate. They already have a complex legacy technology estate to move into the cloud. But as Capital One showed us, migrating an established legacy footprint to the public cloud is possible — it just requires the right approach.

Successful transformation of legacy banking technology hinges on a bank’s ability to do three things:

Reduce the scope of the transformation by deprioritizing capabilities and features that provide diminishing returns

Source undifferentiated capabilities off the shelf, instead of wasting resources on building and maintaining them in-house

Execute an incremental and iterative, value-centric transformation plan that prioritizes the rapid delivery of ROI to the business — cutting risk at the same time

Successful cloud-native transformation of a traditional bank

Thoughtworks helps incumbent banks to overcome the challenges they face when modernizing and transforming their legacy systems, by taking an iterative and incremental approach to cloud adoption.

Our approach is designed to generate business aligned momentum. By migrating capabilities incrementally, we enable businesses to quickly see the value of cloud transformation, building and multiplying their motivation for transformation over time. This motivation then helps secure program funding that helps maintain that momentum, creating a flywheel effect as shown in the diagram below:

The Tranformation Flywheel

One of the keys to successfully achieving this flywheel effect with cloud nativity is incrementally transforming systems into modular and decoupled services that are tightly aligned with business capabilities.

These services interact with each other using well-defined APIs, like lego blocks, which come together to enable composability across banking systems — empowering banks to quickly add and remove capabilities as required, without disruption.

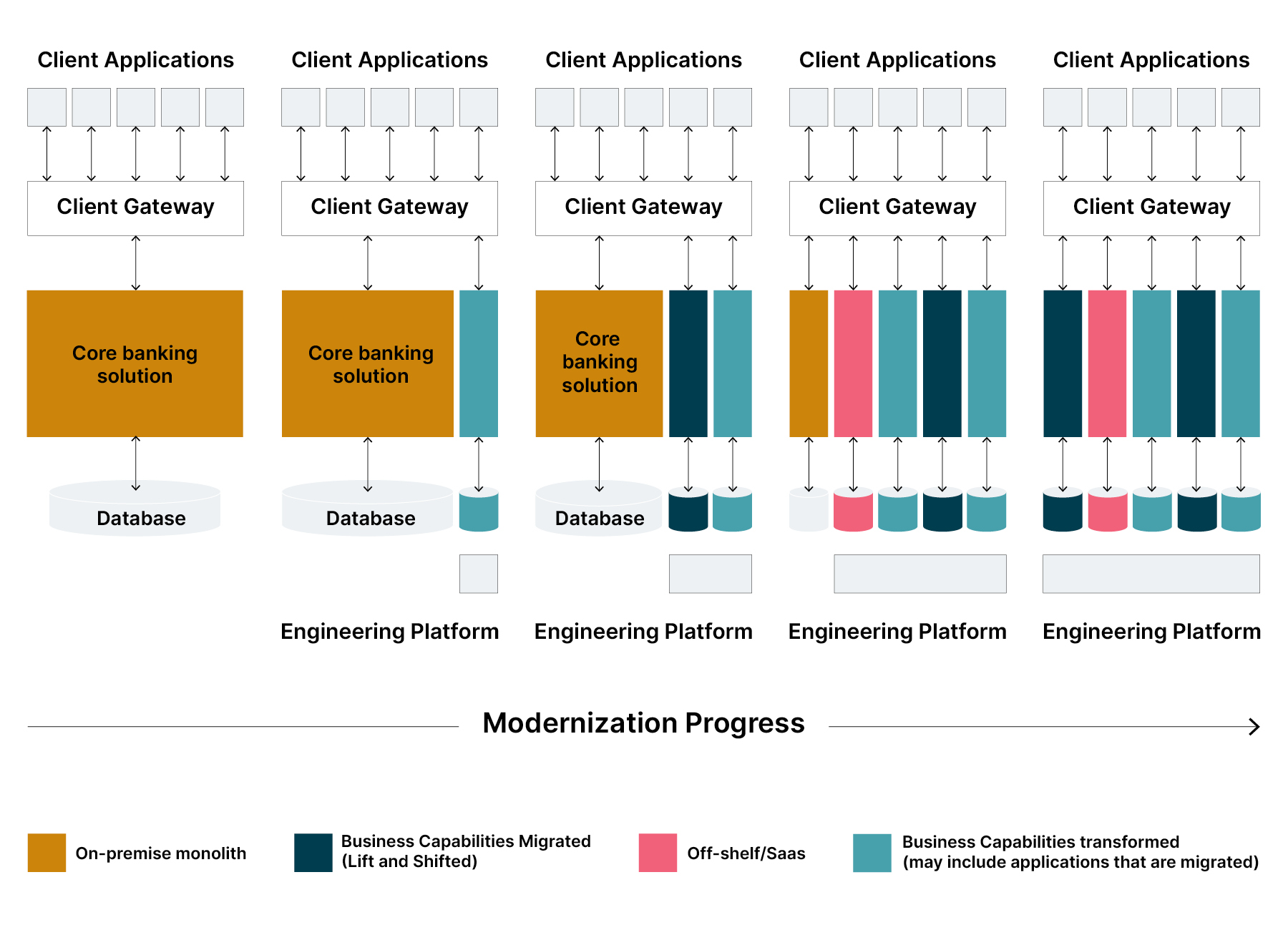

The diagram below shows what that incremental transformation looks like. Over time, the core banking solution is broken down into modular services. These can easily be reconfigured, switched out or swapped without disrupting other essential capabilities:

Cloud transformation of a core banking system

How to create composable cloud-native banking technology that drives business success

When we help banks to embrace composable, cloud-native banking, we consider nine key areas:

Considerations for composable cloud native banking technology

Going beyond trust and financial sustainability to embrace entirely new business models.

In addition to helping banks build the trust, agility, and financial sustainability they need to succeed, composable cloud-native banking has also helped create two entirely new business models to unlock new revenue streams and acquire digital capabilities with minimal overheads.

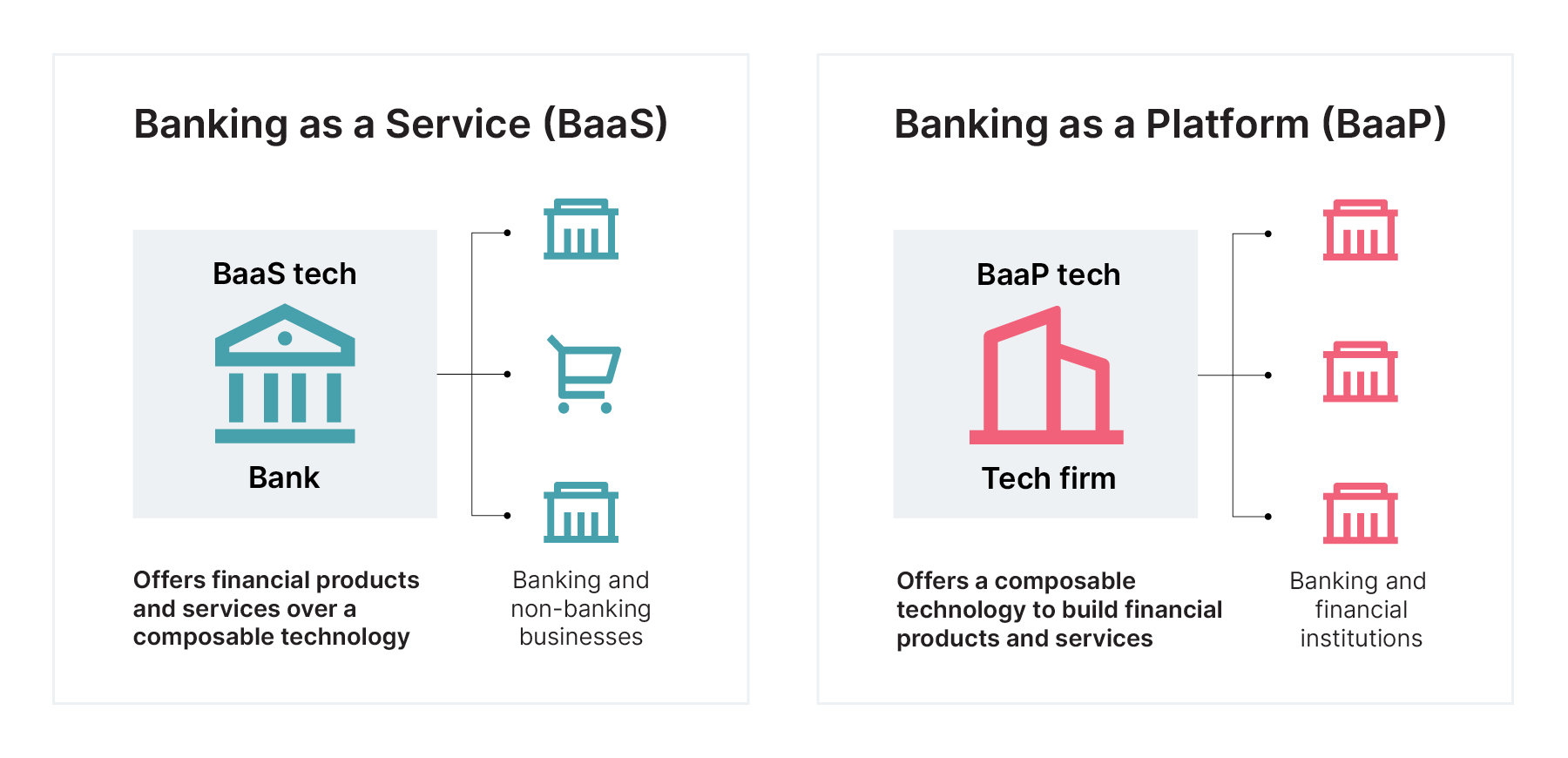

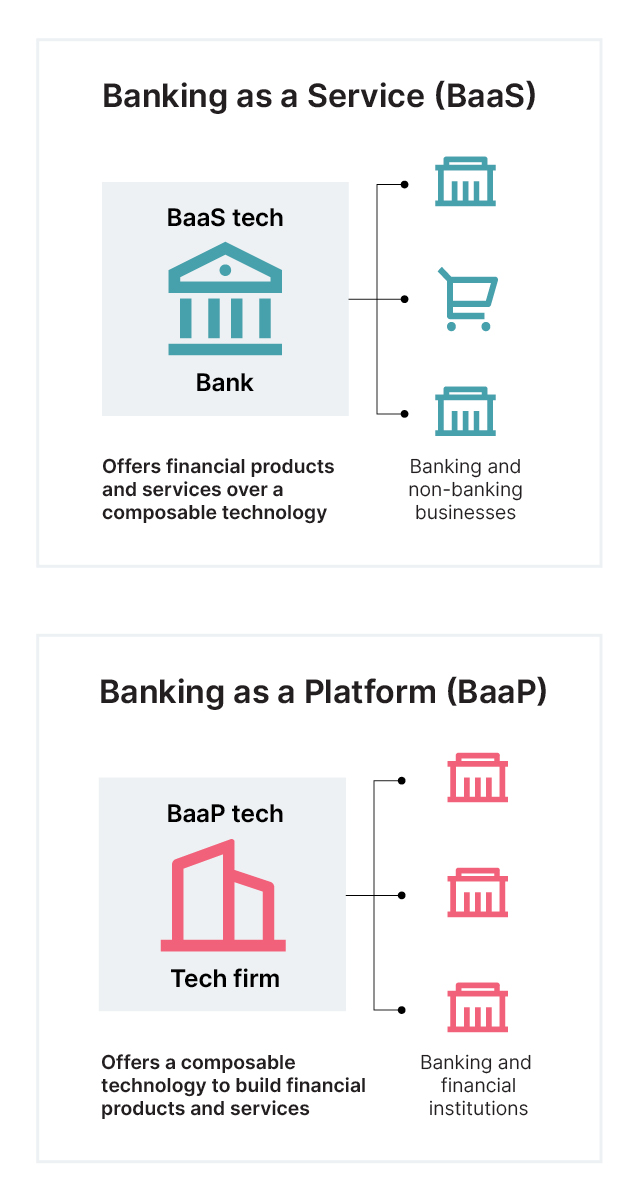

The first is Banking as a Platform (BaaP). In BaaP, non-banking entities provide technology platforms and services to banks and financial institutions, preferably as self-service in a digital marketplace.

The second is the inverse — Banking as a Service (BaaS). In BaaS, banks enable both banks and non-banking companies to market financial products and services using their technology.

New banking business models - BaaS and BaaP

Together, these models are transforming how banks acquire digital capabilities and grow their business, at times exponentially. BaaP reduces a bank’s lead time to value with SaaS technology. BaaS enables banks to turn their technology into a whole new partnership driven revenue stream.

Cloud-native banking is within reach. Make it a reality for your organization today

The public cloud is perfectly suited to the needs of today’s banks. If you’re one of the thousands of banks that have seen cloud transformation efforts grind to a halt, don’t let your journey end there.

By taking an incremental, value-driven approach to public cloud transformation, your organization can drive customer trust, save money, bring new services to market faster and respond to shifting consumer needs at speed.