Digital innovation

Escaping the Tame Corners of Innovation

“If I wish to engage, then the enemy, for all his high ramparts and deep moat, cannot avoid engagement.” - Sun Tzu

How frightening should the prospect of disruptive innovators be for the leaders of a well-run business? There’s a reason for skepticism. Even with all the talk of innovation and creative change in the global marketplace, for many years business success has depended as much on defending against change as enabling it.

There’s a long history of walls and moats protecting established enterprises from the rabble of insurgent competitors, with security in size and experience giving market leaders the confidence of kings safe in their high keep. While the media coverage goes to firms with cool new technologies, many industries have sustained the position of their leading firms by incrementally adopting advances from within the safety of proven market defenses. Is there a reason to believe those walls are failing after so many years of good service sustaining the status quo?

Something is certainly going on. There are those like Klaus Schwab of the World Economic Forum who see this as the cusp of a new era, where disruptive innovators rush into the world’s markets, driving a “transformation that will be unlike anything humankind has experienced before.”

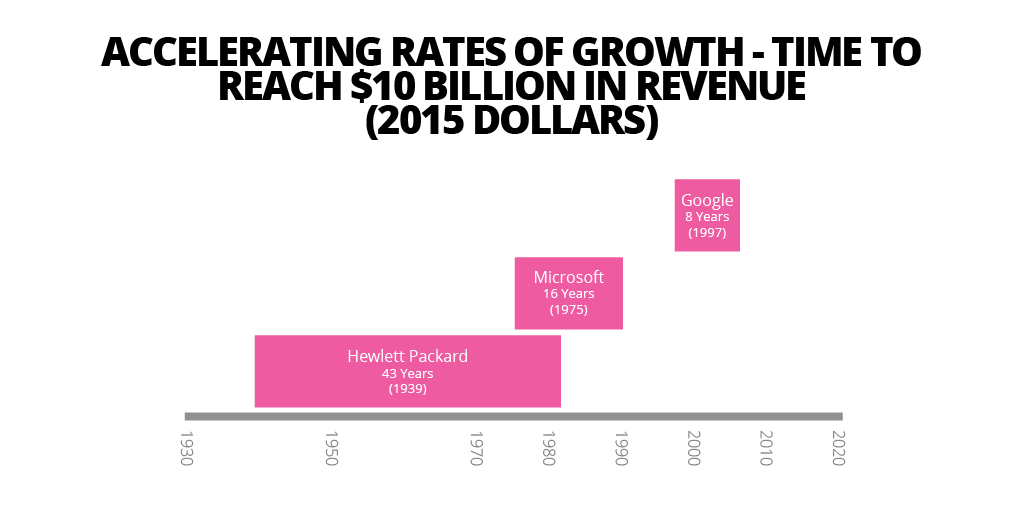

There’s been a notable acceleration of the business lifecycle, with new businesses achieving scale at progressively faster rates. The leaders of technology birthed in the 20th Century were able to cut the time to reach $10 billion dollars in revenue from decades to years.

It’s become a commonly cited truism that the time a successful firm spends in the Fortune 500 has been shrinking. These are troubling, but seemingly slow motion shifts in the competitive landscape. The simple acceleration of the business lifecycle doesn’t in itself make disruptive competitors any more threatening. To understand this new danger, it will be necessary to look at individual stories of industries that have experienced not a slow increase in the pace of their evolution, but a quick, devastating overwhelming of defenses that have long been impregnable.

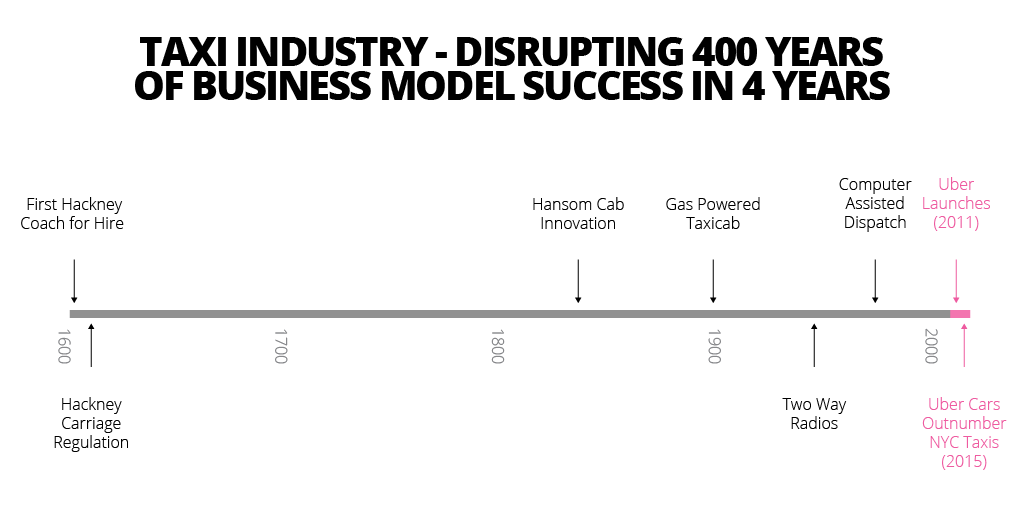

Much has been written about Uber, but to appreciate the story fully it’s necessary to look back at an industry with a long history of business model stability. The taxi business traces its roots to renaissance England and the reign of James I. The first public hackney coach was documented in 1605 and was legally regulated as early as 1635. Licenses were first issued in 1662, and so 70 years before the birth of George Washington, the foundations of the taxi industry were already in place.

Technology augmented rather than disrupted this business model. Joseph Hansom patented the Hansom Cab, providing improved speed and safety for horse drawn carriages. Gottleib Daimler introduced both gasoline powered cabs and the taximeter just before the turn of the 20th century. Over the next 80 years, incremental technology improvements focused on operational optimization, including two way radios (1940s) and computer assisted dispatch (1980s).

Four hundred years of successful business operation made this a highly sought after business opportunity. The walls around the business were substantial. Regulatory barriers constrained entry into the market so a New York City taxi medallion, the right to operate a single cab in New York, could fetch a record price of $1.4 million dollars in 2013. This high initial capital cost was combined with substantial operating expertise needed to manage a large, transitory workforce and maintain a fleet of vehicles in hard use. As a result, with walls and moats in place, innovations crept along.

There was no disruptive technology immediately on the horizon, which makes the sudden, strong challenge to the industry by an upstart that came seemingly out of nowhere all the more amazing. The official launch of Uber was in San Francisco on July 5, 2010, followed by New York, Chicago, Washington, DC and Paris. By March 2015, the number of Uber cars operating in NYC surpassed the number of medallion cabs (14,088 versus 13,587). By year end there would be over 1 million active Uber drivers working in over 300 cities, and the 1 billionth Uber trip would be taken in England.

It took just five years to undermine a business model with a history of four hundred years of success. What happened? We are used to disruption driven by the emergence of a technology that makes old products and services obsolete. No one uses fax machines because email is a vastly superior offering. Physical media content such as CDs, newspapers and print encyclopedias are all trumped by the inherent superiority of digital innovations in their space.

Technology can kill. Yet, it’s easy to assume that exceptional, unpredictable dangers from a subversive shift in technology are an unlucky bullet that happens to hit home. It’s seen as a rare danger, so leaders can remain confident in the capacity of the moats and walls built around their business to defend them from competitors.

This complacency is misplaced. Technology plays a part, but it is not disruption’s only driver. Today, innovators can attack a broad range of opportunities by reimagining foundational aspects of business ecosystems that support scale, including marketing, manufacturing, logistics and product design. They are empowered to to blow up established business ecosystems. Let’s look at three ways they use this capability to turn venerable industries into vulnerable businesses.

Back to the story of Uber. Although there is some controversy as to whether or not Uber is a “disruptor” in the academic sense, it’s hard to think of many other companies that have impacted so many people, in such a wide geographic distribution, in such a short period of time.

Yet, although Uber is often looked at as a classic Silicon Valley “tech startup,” Uber has no technical silver bullet. They didn’t invent flying cars, nor did they pioneer the foundational technologies that make the service possible (mobile GPS, digitized maps, mobile payments, etc.). What they did was create a new ecosystem. This is a different type of disruption, one that circumvents the traditional walls and moats that businesses have relied on to protect their business positions.

At their core, businesses are ecosystems. They connect elements in ways that create market value in a particular way. Traditionally, competition has operated within the established value ecosystems of each market. An improvement might be made in the performance of a particular node or link in the chain, but the overall structure of value creation remains intact.

This creates barriers to entry because established firms can optimize their performance at scale and lay defenses around any possible point of casual entry (e.g. the requirement of taxi medallions to operate a cab in New York City). That explains the stability of the business model for four centuries.

What Uber leveraged was a different kind of technical power. Uber’s founders Garrett Camp and Travis Kalanick didn’t compete within the premises of the established ecosystem. They avoided the need to buy and maintain cars by changing the assumption that vehicles were owned by the firm. They used readily available mobile technology to find a middle ground between hail on the street taxis and far more expense limousine operations. They circumvented the need for taxi medallions and the burdens of fixed assets that might only see use during periods of peak demand. Their ecosystem was constructed out of different assumptions and readily available technology.

Uber versus the taxi industry is a battle of business ecosystems. Uber has clearly won with a superior product. Of course things are not all sunshine and roses for the firm. There are legitimate concerns with the fairness of the labor model and there have been sometimes successful regulatory defenses mounted in some cities, with more likely to come. New competitors like Lyft have introduced competition within Uber’s ecosystem, aiming to compete on traditional grounds by optimizing execution and lowering prices.

Also troubling for Uber is the emergence of new disruptive ecosystems based on self driving cars. Here genuinely original technology will enable new business ecosystems that will likely make Uber’s creative new ecosystem obsolete in less than 20 years. In this new fight, they will face established industry players (GM, BMW, etc.), large, new entrants into the field (Apple, Google) and most likely a few companies that we haven’t heard of (and may not yet be formed).

Ford Motor Company’s Rouge Plant looms over the southern outskirts of Detroit. A huge, integrated factory operation indicative of the advantages of scale in the automotive industry, the plant has its own electrical plant, steel mill, and over 100 miles of interior railroad track. And yet, since the 2003 entry of Tesla into the field, disruptive competitors have shown that the ability to manufacture at scale is no longer protection on its own.

What makes this indifference possible is an increasing digitalization of the product automotive companies sell. Elon Musk has described his flagship car, the Tesla Model S, to be “a very sophisticated computer on wheels”, making Tesla “a software company as much as it is a hardware company.” This was brought home when in the fall of 2015, Tesla upgraded cars currently in operation with new self-driving capabilities. This wasn’t a feature added to new product offerings. It was a software update.

As more of the value of products is lodged in digital systems, new rules govern scale. Firms that can scale their creative efforts have the advantage. This makes sense of both Google’s and Apple’s credible entry into an industry that would have ridiculed their presumption just a few decades earlier. As cars become increasingly digital, the key differentiators will shift to capabilities in software engineering, user experience, upgradeability, mapping, and machine learning. These have not been seen as core capabilities of established automotive firms.

At the same time, traditional manufacturing strengths are becoming ever more commoditized and accessible through third party providers. In the past the cost of setting up design, manufacturing and distribution capabilities at scale was so great that it prohibited new entrants. Electric/digital cars don’t face the same barriers. Driven more by software than mechanical systems, they require two thirds fewer moving parts. So while the costs of scaling up auto manufacturing aren’t low, just look at the investment required to get Tesla to today’s scale, they are far more manageable than they were just 15 years ago.

Digital products and services can replace many offerings in many industries. Advice-based businesses such as healthcare and financial services are also ripe for the digitization of their service offerings. Once the break is made, removing the constraint that scale is dependent on hiring more highly skilled professionals, the door will be open to innovators who can imagine new business ecosystems for promoting health and building wealth.

Intellectual property or other proprietary arrangements are often a final bastion of defense for firms seeking to keep competitors at bay. Patents and proprietary business arrangements defend key junctions in the business ecosystem, blocking the way for others who might hope to reach customers.

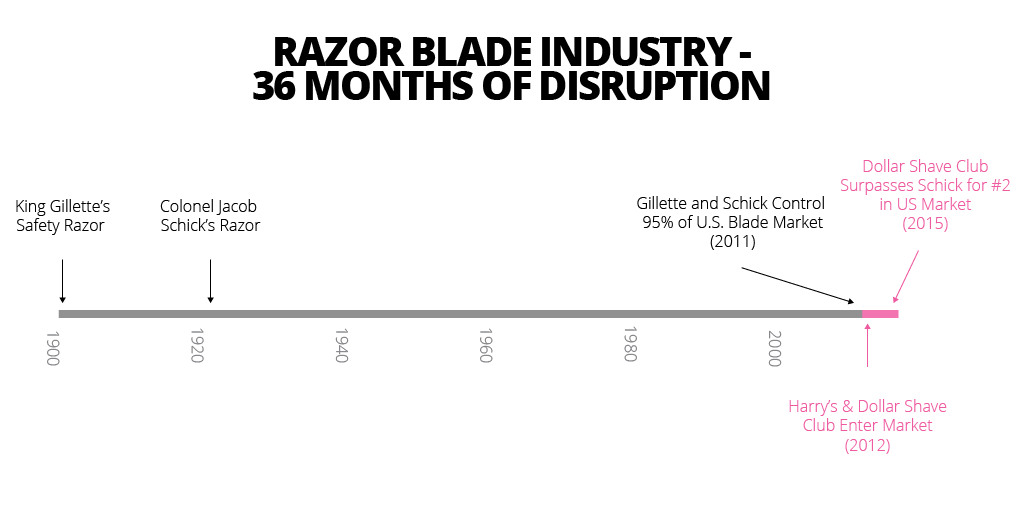

This of course assumes that the competitor can’t simply take a different road, going around rather than through the point of contention. This is the situation that developed in the razor blade industry. In 1901 King Gillette introduced his innovative safety razor, followed in 1921 by Colonel Jacob Schick with his own design. Over the next 90 years Schick and Gillette consolidated over 95% of the market share in the multi-billion dollar US razors and cartridges market. Deep retail relationships and manufacturing capabilities supported their seemingly unassailable dominance.

Inventing an alternative production and market ecosystem would seem to be a fool's quest. Yet in 2012 Harry’s and Dollar Shave Club were formed leveraging outsourced manufacturing, low-cost digital marketing, and online-first sales strategies with clever social media usage (see the original DSC videos done by the CEO, which went viral). Once again they did not reinvent the razor, they reinvented the razor business ecosystem. 2015 online razor sales are estimated at $263 million, with Gillette claiming only 20% (vs 60% in the traditional retail market), and in September 2015 Dollar Shave Club passed Schick to become the second best selling razor cartridge in the US.

By the end of 2015, 2.2 million subscribers had participated in Dollar Shave Club’s ecosystem, which they were able to cobble together around the entrenched position of Gillette and Schick in the space of months not decades.

The digital sales channels these insurgents leveraged were already well developed alternatives to traditional retail. Now even more powerful alternatives to side step market positions exist with the introduction of context-aware Internet of Things (IOT) devices and the intelligent engagement driven by Big Data. Maker technologies that enable customized “printed” products are another powerful tool for turning barriers into mere obstacles. As the cost and effort required to conceive, design, manufacture, and market a product declines, the pace and scale of disruption can only increase.

The walls of scale have crumbled. The moats of proprietary position are drying up. The threat from disruptors is real and when the attack comes it is likely to be in the form of a new business ecosystem that creates an entirely new basis for opportunity. Sweeping away 100 years, or even four centuries of stability, is now the work of a few years or even months.

Upstarts and insurgents aren’t throwing themselves against the walls of the scaled-up enterprise. They don’t need to. They can invent an entirely new market ecosystem that changes the rules and the possibilities in a market. That’s complex work, but its empowered by an ability to digitize products that replace the powers of scale with prowess at innovation. Even the strategically defended barriers based on IP or market relationships lose their power when disruptors can simply leverage new technology and market alternatives to circumvent them.

So what should established companies do? Digging the moat deeper or building the walls higher may delay the competitive threat, but it won’t prevent it. Deep market disruptions from new business ecosystems are inevitable, but being a victim of this disruption is not. Companies must adopt strategies that allow them to respond to disruption more quickly and effectively, or more ambitiously, to be disruptors themselves.

Google calls these “other bets”, innovations that go beyond incremental improvements to existing products. Doing other bets, blowing up ecosystems, is a new and different skill, one that requires abandoning the castle with its illusion of safety by developing a focus on constant reinvention and the pursuit of new business ecosystems.

But how?

To disrupt on the outside, companies must first be disruptive internally. They must abandon long, inflexible planning cycles, drive decisions based on measurable outcomes vs. politics (“selling” in the Lean Startup context), and accept that the only constant for any organization, even in the near-term, is rapid, unrelenting change. Rather than attempt to predict the future, companies should be built to seize the opportunities the future brings, whether planned or totally unexpected.

Disclaimer: The statements and opinions expressed in this article are those of the author(s) and do not necessarily reflect the positions of Thoughtworks.